Is a 2024 Fed Pivot on Interest Rates Coming? What It Means for Your Wallet

For the past two years, the Federal Reserve’s series of interest rate hikes has felt like a constant shock to the system for many Americans. However, a recent a statement from New York Fed President John Williams has signaled a potential shift in monetary policy, suggesting that the era of aggressive rate increases may be coming to an end.

Williams’ careful phrasing about “room for a further adjustment” hints that the Fed may soon consider pausing or even reducing the federal funds rate. For consumers and investors, this is the most significant sign yet of a potential 2024 economic outlook that includes looser borrowing conditions.

Decoding the Fed’s Pivot: A Shift in the 2024 Economic Outlook

For nearly two years, the Federal Reserve’s primary weapon against soaring inflation has been to aggressively raise interest rates. The strategy, often described as “higher for longer,” aimed to cool the economy and stabilize prices. This made borrowing for major purchases like a home, car, or business expansion significantly more expensive.

Now, Williams’ suggestion that a reduction in borrowing costs could happen “in the near term” marks a clear pivot. This indicates the Fed’s confidence is growing in their ability to manage inflation without triggering a deep recession. The conversation is shifting from rate hikes to the possibility of a rate cut, signaling a major change in the interest rate forecast.

The Balancing Act: Why the Fed Might Adjust Its Strategy

The Federal Reserve operates under a “dual mandate”: to maintain stable prices and achieve maximum employment. With inflation showing signs of cooling, the Fed’s focus is expanding to ensure the labor market remains strong.

As Williams noted, the risks to the economy are becoming more “balanced.” This means the danger of causing a recession by keeping rates too high is now as much of a concern as inflation itself. The ultimate goal is a “soft landing”—curbing inflation without causing widespread job losses. Williams’ comments suggest he is increasingly confident in achieving this delicate balance, a key factor in future financial planning.

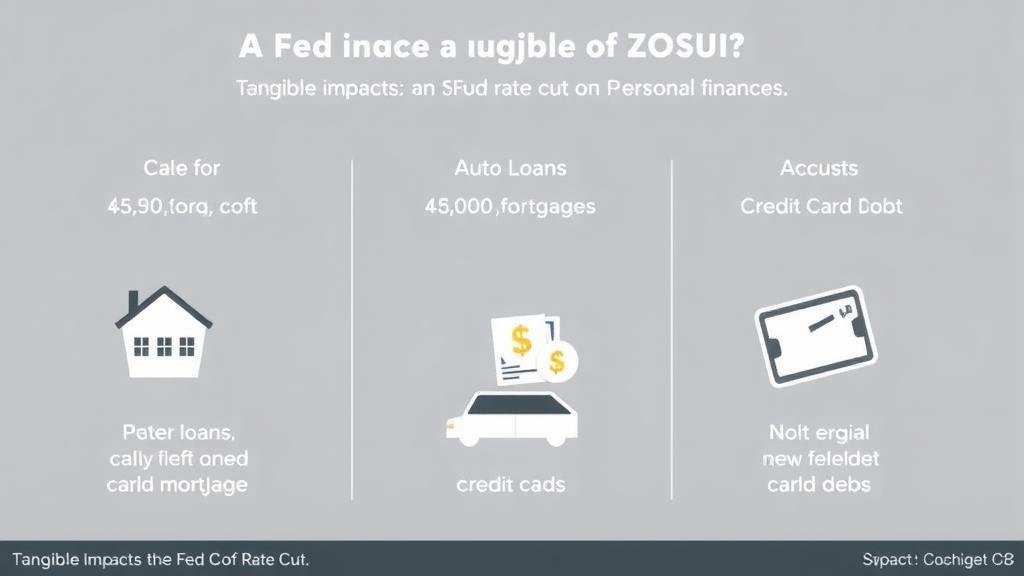

How a Fed Rate Cut Could Impact Your Finances

What does a potential adjustment to the federal funds rate mean for your personal finances? Here’s a breakdown of the potential effects.

Mortgage Rates

The housing market has been particularly sensitive to the Fed’s rate hikes. A policy pivot could provide welcome relief. If the Fed cuts rates, mortgage rates are likely to decrease, making homeownership more affordable and offering an opportunity for current homeowners to refinance.

Auto Loans

Lowering the federal funds rate typically leads to more competitive auto loan rates. This could reduce the monthly payment on a new vehicle, making it more manageable for consumers.

Credit Card Debt

Credit card annual percentage rates (APRs) are directly tied to the Fed’s benchmark rate. The recent hikes have made carrying a balance incredibly costly. A rate cut would be a significant benefit, reducing interest charges and making it easier to pay down high-interest debt.

Savings and Investments

The impact on savings is mixed. While the high rates on high-yield savings accounts might decrease slightly, the stock market often rallies in response to rate cuts. A monetary policy that fosters economic growth is generally seen as positive for investment portfolios.

A Note of Caution: Stay Focused on Financial Planning

While the prospect of lower interest rates is encouraging, it’s important to remain cautious. Williams’ comments are a signal, not a guarantee. The Fed’s decisions are data-dependent, and if a key indicator like the Consumer Price Index (CPI) shows a resurgence in inflation, they could delay or reverse course.

The wisest approach is to continue focusing on sound financial fundamentals. This includes building an emergency fund, paying down high-interest debt, and aligning your investment strategy with your long-term goals.

The Road Ahead: What to Watch in the Coming Months

All eyes are now on upcoming Fed meetings and key economic reports. The Consumer Price Index (CPI) will be a critical indicator of inflation trends and will heavily influence the Fed’s next move.

John Williams’ recent remarks have provided a hopeful glimpse into the 2024 economic outlook. While the future remains uncertain, the possibility of a break from relentlessly high borrowing costs is a welcome development for consumers and a reminder that economic trends can and do change.