From Binge to Balance: Your Guide to Financial Wellness in a World of Impulse Buys

It’s Friday night. You’re on the couch, deep into a crime documentary, and suddenly you’ve eaten a whole bag of chips. How did that happen? Next thing you know, it’s 3 AM, and you’re weirdly invested in the lead detective’s love life. Welcome to binge culture. But that little voice whispering “just one more episode” has a cousin who’s screaming from your online shopping cart, “YOU DESERVE THAT GIZMO!”

In an age of one-click buys and “Buy Now, Pay Later” (more like “Buy Now, Freak Out Later”), our bank accounts have become a free-for-all for impulse buys. So, let’s get real about why your wallet is feeling a bit light. We’re diving into the psychology of our gotta-have-it-now world, the real damage it causes, and how you can break free and achieve financial wellness.

What is Binge Culture and Why Is It Draining Our Bank Accounts?

Remember when “binge” was a word you only whispered to your doctor? Now, it’s a marketing slogan. Netflix practically dares you to sleep, and DoorDash knows you crave spicy tuna rolls on a rough day. This non-stop push for “more, now” has rewired our brains for instant gratification in all aspects of life, including our personal finance.

Honestly, I blame technology and convenience. It feels like a setup, right?

- On-Demand Everything: We’ve gone from waiting a week for the next episode to having entire seasons dropped on us at once. Same-day delivery has erased the “cooling-off” period our parents had. Can you imagine them having to mail-in an order form and a check? The horror!

- The Social Media Effect: Let’s be honest, Instagram is basically a personalized, talking catalog. Influencers unbox “hauls” bigger than a small car, and suddenly your perfectly good coffee maker seems ancient. The fear of missing out (FOMO) grabs you and drags you to the checkout.

- Shopping as a Game: E-commerce sites have turned spending into a game. “LIMITED-TIME OFFER!” flashes on screen. “ONLY 3 LEFT!” a countdown timer pressures you to act NOW before that alpaca-wool sweater is gone forever. “Add to cart” isn’t a choice anymore; it’s a reflex, a quick dopamine hit to numb the pain of a Tuesday afternoon.

The Financial Black Hole of Binge Spending

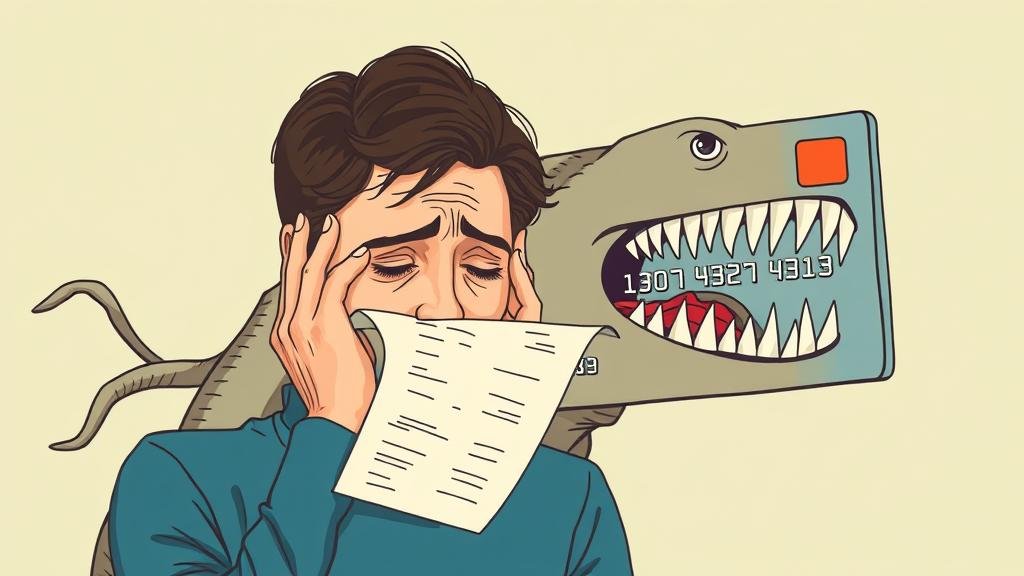

That $20 impulse buy on artisanal pickles might not seem like a big deal. The $50 “treat yourself” sweater is just a little reward. But small leaks sink big ships. The true cost of binge spending isn’t one purchase; it’s the heart-stopping total on your credit card statement that makes you question everything.

Now, before you zone out, let’s look at the science. A study in Behavioral Sciences (yep, I read it for you) found that modern payment methods create “reduced psychological friction.” Tapping your phone feels less real than handing over cash. This phenomenon, which some call “Spendception,” is like something out of a movie. But instead of a dream-heist, it’s Amazon sneaking an air fryer into your cart. For Gen Z, who grew up with this, it’s even more ingrained.

This leads to some not-so-great outcomes:

- Mounting Credit Card Debt: Binge spending is a fast-track to high-interest rates and low vibes. That small balance you were “definitely going to pay off” suddenly brings its scary friend, Compound Interest.

- The Buy Now, Pay Later Trap: Services like Klarna and Afterpay are like free samples for your finances. They’re tempting, but they’re still debt. Miss a payment, and you’ll face fees and a blemish on your credit report. We’ve seen it happen time and time again.

- Ignoring Financial Goals: Every dollar spent on something you didn’t really need is a dollar that could’ve gone into your emergency fund, a down payment on a house, or investments for your future. Binge spending is stealing from Future You, and Future You is not going to be happy.

The Psychology of the Impulse Buy: Why Can’t I Stop?

To stop binge spending, you have to understand it’s rarely about the thing. It’s about the feeling.

Emotional Triggers

My credit card and I have been through some things. I’ve learned we often shop to cope.

- Stress and Anxiety: Tough day at work? Buying something can feel like a small moment of control in a chaotic world.

- Sadness or Boredom: The thrill of a new package can be a temporary cure for the Sunday blues. I once bought a mushroom-growing kit out of pure boredom. (It didn’t end well for the mushrooms.)

- Celebration: We’re conditioned to reward ourselves with things. Nailed a presentation? Time for a splurge! Survived another Monday? Splurge!

This isn’t just a personality quirk; it’s psychology. Our emotions are in the driver’s seat of our financial car, and sometimes they’re headed straight for the mall.

Environmental Cues

Your surroundings are a minefield of spending triggers. Unsubscribing from those 57 daily marketing emails is an act of self-care. Unfollowing accounts that just show you stuff to buy is like giving your brain a much-needed break.

How to Break the Binge-and-Spend Cycle: 5 Missions to Reclaim Your Financial Wellness

Regaining control isn’t about deprivation; it’s about being intentional. It’s about becoming the boss of your money.

- The 24-Hour Rule: Call it the “Marination Mandate.” See something you want? Put it in your cart and walk away. For a full 24 hours. Let that impulse cool off. You’ll be surprised how often you come back and wonder, “A lamp made of old bowling pins? Was I okay yesterday?”

- Mindful Money Tracking: You can’t change what you don’t measure. For one month, track every single dollar. Use an app, a spreadsheet, or whatever works for you. Facing your financial reality can be scary, but it’s the only way to see what’s really going on and start your journey to personal finance mastery.

- The “Fun & Future” Budget: This is my favorite. Set up a dedicated fund for guilt-free spending. This is your “fun” money. Once it’s gone for the month, it’s gone. At the same time, automate transfers to your savings and investments—your “future” fund. Pay your future self first.

- Identify and Replace Your Triggers: Next time you feel the urge to binge-shop, pause. Ask yourself, “What am I really feeling?” Bored? Call a friend. Stressed? Go for a walk. Anxious? Watch a funny cat video. Replacing shopping with a healthier habit is the ultimate life hack.

- Make Spending Harder: Add back some of that “psychological friction.” Unsave your credit card info from websites. Delete shopping apps from your phone’s home screen. If you’re feeling brave, switch to cash for problem spending areas. Handing over five $20 bills for a $100 pair of jeans feels much more significant than a silent tap.

From Binge to Balance ⚖️

The culture of binge spending promises instant happiness but usually just leaves you with a closet full of unworn clothes and a lingering sense of dread. Sound familiar?

Breaking free isn’t about living like a monk. It’s about choosing intentional living over mindless consumption. It’s about trading the fleeting joy of “add to cart” for the deep satisfaction of financial security.

Building wealth isn’t about one big move; it’s about the small, smart decisions you make every day. And yes, this will be on the test. The test is your bank account at the end of the year.